About Square Textile Ltd.:

Square

Textiles Limited has started its journey by establishing the first unit in

1997. One year later the second unit was established. Square Textile is a

subsidiary company of Square Group .The Company was incorporated as a public

limited company in the year of 1994. The operation was started in 1997.It was

enlisted in Dhaka Stock Exchange & Chittagong Stock Exchange in 2002.

Within a very short time of span the company achieved some significance

success. Square Textile receives Oeko-Tex standard 100 and ISO-9002

certificates in the year 2000. Authorized capital of the company is tk. 1000

million. It’s paid- up capital is tk. 251.90 million. 1,223 employees are

working in this organization. The business lines of Square Textiles Limited are

manufacturing and marketing of yarn. The factory is located in Saradaganj,

Kashimpur, Gazipur, Bangladesh. Its office is located at Uttara in Dhaka. Its

main objective is to strive hard to optimize profit through conduction of

transparent business operations within the legal and social framework with

malice to none and justice for all.

Rationality of Study:

This

Assignment is on different financial analysis of Square Textiles Limited. here,

different financial analysis is conducted to find out the actual position of

the company in the current market situation. In this Assignment, ratio analysis

cost of money and stock valuation is conducted to find the right decision.

Financial &

Operational Highlights:

Liquidity Ratios:

Liquidity ratio measures the firm’s ability to meet its

obligations, ability to pay its obligation and when they become due. These

ratios establish relation between cash and other current asset and current

liabilities. Commonly used ratios are

·

Current Ratio

·

Quick Ratio

1.

Current Ratio:

Current Ratio shows the

proportion of current assets of a business in relation to its current liability

Current Ratio = Current Asset /Current

Liability

Standard

=2:1

Analysis: The

current ratio measures the company’s ability to pay off its current liability.

Here we can see that current ratio was highest in 2012 with compare in

preceding years. We know standard of current ratio is 2:1. It means a current

ratio 2 means that current asset asr sufficient to cover for twice the amount

of a company’s short term liabilities and then it is considered to have good

short term financial strength. But I 2012 Current Ratio is above 2, so it denotes

that CR Liquidity company has idle money, so it is not good

sign for the Square textile Ltd. So in a concluding note I would like to say

company should utilize their idle money in a profitable manner.

2.

Acid Test Ratio :

The Acid test or quick ratio or liquid

ratio measures the ability of a company to use its near cash or quick assts to

extinguish or retire its current liabilities immediately.

Acid Test = Current Asset – Inventory

/Current Liability (times)

·

Standard = 1:1

· QR Liquidity

Analysis:

Quick ratio is the most conservative ratio

in calculating liquidity position. A company with a quick ratio of less than 1

can not currently pay back its current liabilities ; it’s the bad sign of

investors .Here we can see that acid-test was not stable in 2008 & 2010 ,

but it was increased dramatically in 2012. The company’s current liquidity

position in 2011 is satisfactory. But too much liquidity is not good. In 2012

it is too liquidity. Which can be a good sign and as well as bad sign.

v Activity /Efficiency / Asset Ratio

Activity ratios are used to evaluate the competence, which

the company manages and utilizes on its asset. This ratio also calls the

turnover ratios because they indicate the speed with which the assets are

transformed or turnover into sales. A proper balance between assets and sales generally

reflects on that the assets.

The Activity ratio we can satisfy on the three ratios,

those are:

- Accounts Receivable Turnover.

- Inventory Turnover

- Fixed Assets Turnover

- Accounts Payable Turnover

- Total Asset Turnover

- Average Collection Period

·

Accounts Receivable

Turnover:

This ratio helps to find out average

collection period of accounts receivables. The lower the collection periods the

higher the management efficiency measure collect the account receivables.

Receivable Turnover = Net Credit

Sales / Accounts Receivable

ART Efficiency

Analysis:

Accounts receivables turnover is measure

the number of times per year that the average amount of receivables is

collected and transfers the cash amount. If the organization account receivable

turnover increase then the average collection period decrease and vice-versa.

Here we see that in 2012 is 2.67 times account receivable turnover Highest and

Average collection period less. In 2012 a high value of accounts receivable

turnover is favorable because it indicates high efficiency and improvement in

the process of cash collection on credit sales

Average Collection Period:

Average Collection Period:

The approximate amount of time that it

takes for business to receive payments owed, in terms of receivable , from its

customer and clients.

ACP efficiency

Analysis:

·

Inventory Turnover

ratio:

A ratio showing how many times a company’s

inventory is sold and replaced over a period.

Inventory Turnover = COGS / Average

Inventory

IT

efficiency

Analysis:

Inventory turnover ratio measures how fast

the inventory become cash or accounts receivable. If the turnover number is

more than the company’s position is good and vice versa. In 2008 it is

2.04 times and in 2009 is 3.55 times in 2010 it is 2.19 times in 2011 it is

3.38 in 2012 3.85. Here we see the turnover is increasing over the time. It

shows a positive impact on their management efficiency.

Inventory Processing period:

The approximate amount of time that it takes for a business to sell &

replace its inventory

IPP efficiency

Analysis:

Average payment period tell about how many

time a company takes to pay its accounts payable. If a company quickly pays the

accounts payable then it means they can’t use their capital properly on the

other hand if it take too much time to pay its accounts payable then it will

hamper their reputation toward its debtors. It wills create problem for further

loan. Here we have seen their average payment period is decreasing over the year.

In 2012 the period slightly decreases then the previous year. The overall

position is good.

·

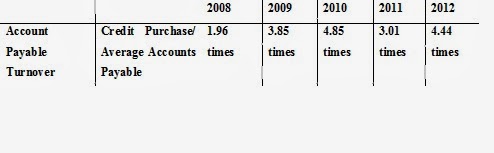

Account Payable Turnover:

Is an accounting

liquidity metric that evaluates how fast a company pays off its creditors (suppliers)

Account

Payable Turnover: Credit Purchase/ Average Accounts Payable

APT

Efficiency

Low value of account payable turnover is

favorable and higher figure may indicate inefficiency. Square company’s payable

turnover increasing over the year it indicates too much inefficiency of the company.

- Average Payment Period:

Average Payment Period means the average

period taken by the company in making payments to its creditors.

Low value of account processing period is

favorable and higher figure may indicate inefficiency. Square company’s payable

turnover increasing over the year it indicates too much inefficiency of the

company.

APP Efficiency

Analysis:

Company’s

total asset turnover is good because it is increasing over the year.

v Profitability Ratio

Profitability ratio represents the organization’s ability

to translate sales dollars at different stages of measurement. The ratio

measures profitability after consideration of all revenues and expenses,

including interest taxes and non-operating items. This ratio specify the

capacity of the company to survive difficult circumstances, which might occur

from a number of basis, such as declining price, increasing coast and declining

sale.

The profitability ratio we can justify on the five ratios,

those are as follows

·

Gross

Profit Margin Ratio

·

Net

profit Margin Ratio

·

Return

on Investment/ Asset Ratio

·

Return

on Equity Ratio

1.

Gross Profit

Margin:

Analysis:

Gross margin ratio is used to analyze how efficiently a

company is using its materials, labor and manufacturing related fixed assets to

generate profits. A higher gross margin percentage is a favorable profit

indicator and vice-versa. This ratio helps organization to fix their product

price. If the ratio minimum percentage then indicates the product market price

lower or product production cost high. Here we see that gross margin ratio was

quite stable in 2010 & 2011 but it fall down 2% in 2012 which can give alarm for Square

Pharmaceuticals Ltd

2.

Net profit margin

Profit Margin= Net Income /Net Sales*100

Analysis:

Net income to sales ratio is very important in operating

performance measurement. This ratio is helpful in identifying the proportion of

sales unit that remains after the deduction of all expenses. This ratio indicates

the net amount of profit on each sales taka. The amount of net income includes

all types of non operating items that may occur in a particular period. The

ratio dropped in 2009, then increase in 2010. But it again fell in 2011.

As a result company has generated less profit than 2011

3.

Return On Asset:

Return on Asset = Net Income /Total Asset.

Asset

3.68% 3.14% 4.92%

5.20%

Analysis:

Return on total assets indicates how profitable a company

is relative to its total assets. It also indicates the management efficiency to

utilize total assets to make profit. In 2011 it has been slightly increased

compared to the previous year. So it can be said that company generates 3.68%,

3.14%, 4.92%, and 5.20% return on the assets that it employs in its operations

in this four year time period.

4.

Return On Equity:

Return on Equity = Net Income /Total

Equity

Analysis:

Return on equity is the measurement of shareholders wealth

maximization. It indicates how much shareholders earned from their investment.

The higher the ratio indicates higher the shareholders wealth maximization.

Return on equity is highest in 2009 return shows 16%. So it’s bad news for

Square Pharmaceuticals Ltd. that its present ROE is decreasing than previous

year.

v Market Measures Ratios

1.

Price Earnings

Ratio :

Price Earnings Ratio = Market Price /

Earnings Per Share0

Analysis:

Price earnings ratio is the most widely used indictors in

investment decision. It indicates how much an investor would be paying for

every taka earnings. Price earnings ratio was height in 2009 but it has

decreasing in 2010. So it means market price of BPL was fall in 2011. In 2012

P/E ratio go up .So company is now growing up & should aware also of their

P/E ratio.

Earnings Per Share

Earnings per Share = Net Income / Number

of Common Stock

Share 46.45 times 37.72

times 32.32times 19.66 times

Analysis:

Price earnings ratio is the most widely used indictors in

investment decision. It indicates how much an investor would be paying for

every taka earnings. Price earnings ratio was height in 2008 but it has

decreasing in 2009. So it means market price of BPL was fall in 2011. So

company should aware of their P/E ratio.

·

Solvency

/Debt Coverage Ratio

Debt ratios are calculated to judgment the long-term This

ratio indicate, mix of funds provided by owners and lenders, the manner in

which the assets are finance, the extent of earning that is magnified or

leveraged by use of debt and finally the extent of limited stakeholders control

over the company.

The Debt- coverage ratio we can satisfy on two ratios,

those are:

·

Debt

to total assets

·

Time interest earned

Debt Ratio: The ratio of total debt to

total assets. It measures the percentage of the firm’s assets financed by

borrowings.

Debt Ratio

Analysis:

Debt

ratio is widely used indictors in investment decision. It indicates how much an

investor has debt against assets. Debt ratio was height in 2008 but it has

decreasing in 2009. So it means market price of BPL was fall in 2011. So

company should aware of their Debt ratio.

Conclusion:

Financial statements of a company are

most important for finding their situation. As a partial requirement of Managerial

Finance this report the ratio analysis of financial statement” has been

prepared.

This report broadens our understanding in

internal control. Though this task we have gained real life experience on Managerial

Finance. By doing this report. We faced some difficulties like secrecy of

information, lack of budget, prior experience etc. So, these are some week ness

in this report. The main objective of this report was to understand and find

out the financial position of Square Textile Ltd.

Bibliography

01. Accounting principal (8th

edition)

02. By Weygandt, Kiso, Kimmel

03. Company

profile

- See more at: http://www.assignmentpoint.com/business/finance/ratio-analysis-of-financial-statement-of-orion-fusion-ltd.html#sthash.8TP6egGn.dpuf

·

Internet Source: Google, Encyclopedia,

Wikipedia.

·

Company website: www.hsbc.bd.org

No comments:

Post a Comment